On May 31, 2024, the European Financial Reporting Advisory Group (EFRAG) published the first implementation guidelines to assist in the application of the EU Sustainability Reporting Standards (ESRS), providing guidance for the disclosure of sustainable development information required by the Corporate Sustainability Reporting Directive (CSRD).

This article aims to enhance companies' understanding of the dual materiality concept and the application of the materiality assessment process through an in-depth interpretation of the first of the first batch of implementation guidelines, the Materiality Assessment Implementation Guidance (MAIG), so as to improve their cognition and practical ability on sustainable issues.

The meaning and explanation of dual importance

01The meaning of dual importance

Double Materiality (also translated as double materiality) includes impact materiality and financial materiality.

Impact significance refers to the actual or potential, positive or negative, significant impact of sustainability issues on people and the environment in the short, medium or long term, covering the company's own operations and the upstream and downstream value chains (generated through products and services or business relationships);

Financial materiality refers to the actual or expected significant financial impact of the risks and opportunities brought about by sustainability issues on the company, including significant impact on the company's development, financial status, financial performance, cash flow, financing availability, capital cost, etc. in the short/medium/long term.

02 Development of dual importance

The concept of dual materiality was first proposed by the European Union in 2017 in the Guidelines on non-financial reporting: Supplement on reporting climate-related information, which requires companies to disclose information related to sustainable development that affects financial performance, as well as information on the impact of corporate production and operations on people and the environment. ESRS follows the principle of dual materiality in this guideline and proposes more detailed and standardized information disclosure requirements for important ESG issues. In addition, ESRS also requires companies to verify the ESG information they disclose and be responsible for the authenticity of the content.

As an application guide for ESRS, the "Guide to Implementation of Materiality Assessment" explains the operation methods and practical cases of dual materiality in more detail, which helps companies better understand the connotation of dual materiality in ESRS. For ESG issues that are confirmed to be of dual materiality after assessment, companies need to further disclose the impacts, risks and opportunities (IROs, hereinafter referred to as "IROs") brought about by the issue, which is also the key content of the EU sustainability statement.

03 Explanation of “Importance”

Impact materiality and financial materiality are closely related and interdependent. Risks or opportunities may arise from a company's strategic changes, investments, and management decisions on its impact on people and the environment. Important risks and opportunities often arise from the company's external impacts and its dependence on nature, human resources, etc. (for example, a law firm may lose employees due to higher salaries offered by local peers under the same circumstances, resulting in a decrease in the firm's income), and most important impacts will generate important risks or opportunities over time (for example, an oil and gas company may fail to reach an agreement with local residents on land extraction and use and resident relocation, causing local residents to launch protests and stop extraction production, resulting in actual economic losses due to delayed delivery or abandoned extraction projects).

In addition, if an enterprise omits, misreports or conceals information on risks or opportunities in its sustainable development report and affects the decision-making behavior of users of financial reports, then these risks and opportunities will be considered financially material. The sources of financially material risks or opportunities are not limited to the parent and subsidiary companies within the scope of the enterprise's consolidated financial statements, but extend to related companies in the entire upstream and downstream value chain, including suppliers, customers and partners.

Figure 1 Important sources of risks and opportunities

The time frame covered by financial materiality often exceeds the time frame defined by a company's single financial reporting cycle and management's explanation. When evaluating the financial materiality of an ESG topic, companies should consider the cumulative changes that may occur in financial effects such as revenue and costs over a longer period of time. Similarly, the probability of occurrence of risks or opportunities related to these topics may also change cumulatively over time. Companies' assessments of financial materiality should not be limited to the scope of traditional financial accounting indicators, but should expand their focus to financial impacts related to reliance on natural and social resources, which are often not fully reflected in current accounting recognition standards. Companies' proactive consideration of such financial impacts will help to more comprehensively assess financial materiality.

Materiality Assessment Process

The "Guidelines for the Implementation of Materiality Assessment" provides a basic step reference for the materiality assessment process (see Figure 2). Enterprises can make adjustments based on actual conditions to compensate for differences in the industry, country, organizational structure, business operations, and upstream and downstream value chains in which the enterprise is located. Enterprises should establish materiality assessment standards and materiality comparison thresholds that are in line with their own characteristics.

Figure 2 Example of materiality assessment process

The materiality assessment process consists of four steps:

Step A: Understand the background information of the company and its main stakeholders

Corporate background information includes corporate economic activities, products/services, and geographic locations where business is conducted. Analyzing corporate business plans, strategies, financial statements, and other information provided to investors, as well as upstream and downstream value chains, types and attributes of business relationships can help companies understand IROs; understanding corporate-specific IROs can be obtained by analyzing corporate-related laws and regulations, regulatory background, and sources of public information such as media, peer analysis, current industry benchmarks, and scientific research reports.

The main stakeholders of an enterprise refer to the entities affected by the business development and upstream and downstream value chains of the enterprise. The situation and demands of the main stakeholders are understood by analyzing the existing stakeholder communication mechanisms (such as dialogue, investor relations, business management, sales and procurement), and the stakeholders are sorted out in accordance with the business activities/relationships, products or services of the enterprise (the corresponding relationship of stakeholders in step A may need to be revised after step B).

Step B: Identify current/potential IROs related to ESG factors

Figure 3 ESRS 1 Appendix A AR 16 List

ESRS 1 Appendix A AR 16 list clearly divides the three-level classification of ESG topics (Topic/Sub-topic/Sub-sub-topics). Enterprises can refer to this list to sort out ESG factors to ensure that there are no omissions. At the same time, they should also consider enterprise-specific ESG factors other than the appendix list. At present, the EU has not yet issued industry ESRS standards, so industry-specific ESG factors can be disclosed according to enterprise-specific ESG factors. Enterprises can use other disclosure frameworks and standards to identify their own unique ESG factors, such as IFRS "International Financial Reporting Standard S2-Climate-related Disclosures" Industry Implementation Guide, GRI "Sustainability Reporting Standards-Industry Standards" , etc. In addition, enterprises can also refer to the "ESRS Data Point List" issued by the European Financial Reporting Advisory Group (EFRAG) to identify ESG factors and important IROs in more detail, although the purpose of the list is to provide data structure support for the digital management of sustainable development reports, rather than for corporate ESG information collection and verification.

Implement the identification methods recommended by the guidelines

Method 1: Companies can first sort out and identify potential ESG factors according to the ESRS 1 Appendix A AR 16 list, and then supplement the company's unique ESG factors according to internal processes (such as due diligence, risk management, and complaint mechanisms) or external processes (such as stakeholder communication and the methods mentioned in step A) to improve them, and finally form a list of corporate ESG factors.

Method 2: Enterprises can directly establish a list of IROs related to their own business model and upstream and downstream value chains in accordance with the reporting process of the GRI Sustainability Reporting Standards and their own internal processes (such as due diligence and risk management), and then check and integrate the three-level ESG themes in the ESRS 1 Appendix A AR 16 list to avoid omissions, and finally form a list of corporate ESG factors. In addition, it is recommended that enterprises refer to the ESRS Data Point List to assist in identifying ESG factors, especially enterprises that disclose sustainability reports for the first time.

Step C: Evaluate and identify significant IROs related to ESG factors

The materiality assessment process starts with the impact of the enterprise on people and the environment, assessing whether these impacts pose risks or opportunities to the enterprise, and then assessing the risks and opportunities caused by the enterprise's resource dependence (for example, the enterprise relies on people and natural resources to conduct its business but the enterprise has no impact on them).

When conducting assessments, companies need to consider the correlation between impact materiality and financial materiality and carry out appropriate and reasonable assessment processes. For example, whether impact materiality assessment and financial materiality assessment should be divided into two independent processes, in principle, it is recommended to integrate the two processes to avoid missing important IROs. The ESRS ESG Theme Standard (i.e., ESRS 1 Appendix A AR 16 Checklist) can provide companies with directions and angles for identifying ESG factors (see Figure 4).

Figure 4 Dual importance assessment

Implement the assessment methods recommended by the guideline

1) Assess the importance of impact

The impacts of corporate ESG factors are divided into positive/negative, currently occurring/likely to occur, and the "materiality" judgment value applicable to the company is determined according to the type of impact (see Figure 5). If the severity of a certain impact has a recognized scientific basis, the company can determine that the impact is "material" without further analysis. Communication with stakeholders who are mainly affected can help companies understand the transmission path of the impact, assess the severity of the impact and the possibility of occurrence. Internal communication between companies and functional departments and employees, and communication with report users and relevant experts can help evaluate , verify and ensure the integrity of the materiality assessment results. The "Guidelines for the Implementation of Materiality Assessment" provides a schematic diagram of the judgment process for determining the materiality of impacts for reference by companies (see Figure 5).

Figure 5: Assessment of impact importance

Figure 6 Judging whether the impact is significant

The severity of the negative impact requires the determination of three factors: level, scope, and whether it is remediable. Level refers to the severity of the impact, such as the degree of infringement on the acquisition of basic necessities of life, the degree of infringement on the freedom of education and the freedom to make a living; scope refers to the affected area, such as the number of people affected and the degree of environmental damage; whether the impact is remediable, such as whether the affected people can regain their rights through return or compensation, or whether the ability to repair the environment is limited and cannot be restored to the time before the impact occurred. Any factor may cause the impact to become serious, and the three factors interact with each other. Whether it is remediable will increase the severity as the level of the impact increases. Conversely, the increase in the level of the impact or the expansion of the scope will make it difficult to remedy. Enterprises can use due diligence procedures or risk management procedures to obtain materiality thresholds, analyze the severity of negative impacts and risk priorities, and determine which impacts are important. Enterprises should give priority to supporting evidence that can draw more objective conclusions and set materiality thresholds based on these evidences.

2) Assessing financial materiality

Significant opportunities and risks are usually generated by impacts, dependencies and other factors (such as climate risk exposure and regulatory changes to address systemic risks). Assessing whether opportunities and risks are significant requires the use of reasonable quantitative or qualitative thresholds (such as financial status, financial performance, cash flow, financing availability, capital costs and other financial impacts). The full text of ESRS discusses risks and opportunities as a whole combination when explaining the reporting disclosure requirements. However, it is worth noting that in certain specific situations, ESG factors only trigger a single aspect of risk or opportunity, rather than necessarily both at the same time.

Figure 7 Assessing financial materiality

When evaluating the opportunities and risks brought by ESG factors, companies need to consider the possibility of opportunities and risks, and the possible financial impact in the short, medium and long term. Companies need to establish objective thresholds for possibility, financial impact and the nature of financial impact, and then judge the possible important opportunities and risks identified in step B one by one; they also need to evaluate whether the impact of ESG factors identified in step B has produced important financial impacts; if the risk management established within the company covers sustainable development risks, the possibility of opportunities and risks and the corresponding financial impact can be further evaluated. Communication with functional departments within the company, corporate investors, and other financial partners (such as banks) can help evaluate, verify, and ensure the integrity of the materiality assessment results.

Enterprises can set an absolute or relative value of the monetary limit (such as the percentage change of a certain indicator in the financial report, such as the income, cost, total assets or net assets), which is close to the importance threshold used to evaluate a certain indicator when preparing financial reports. If an ESG factor is financially important but the financial impact it causes cannot be accurately measured when the report is issued, the enterprise can refer more to qualitative factors and factors of the probability of occurrence to determine the importance threshold. In addition, the qualitative assessment of the importance threshold also includes the following situations: Enterprises may have reputation risks that investors are concerned about because they are engaged in multiple industries or have unique business models. Although the financial impact on cash flow cannot be quantified, reputation risks will cause changes in financing costs and financing methods, which will also be deemed to be financially important.

3) Integrate the evaluation results

The company integrates the results of the assessment process from step A to step C to form a list of important IROs to prepare for the disclosure of the sustainable development report. Analyze the important three-level (theme-sub-theme-sub-theme) ESG issues to ensure that they are all converted into IROs. The individual impacts, risks, and opportunities assessed by the company based on appropriate materiality thresholds and methods need to be appropriately integrated in accordance with the relevant requirements for report disclosure, and the results of the integration must be confirmed with the company's management, in order to fully reflect the company's important IROs.

Step D: Disclose the evaluation process and results of important IROs in accordance with ESRS requirements

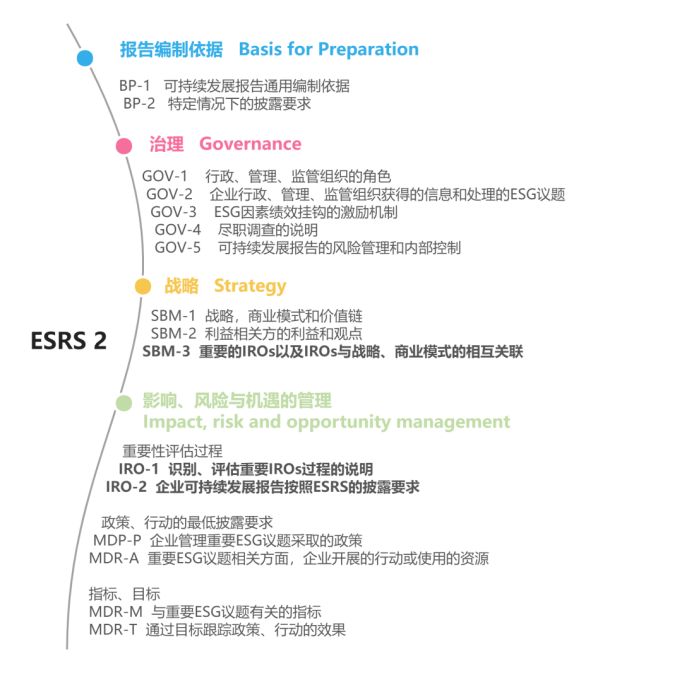

ESRS 2 is the disclosure requirement for the EU CSRD sustainable development report, which is divided into the following four parts: basis for report preparation, governance, strategy, and management of impacts, risks and opportunities (see Figure 8).

Figure 8 ESRS 2 content

Among them, there are three disclosure requirements involving dual importance (the bold part in Figure 8), namely, the disclosure of the identification process and evaluation process of important IROs (IRO-1), the relationship between important IROs and corporate strategy and business model (SBM-3), and the explanation of the disclosure of important IROs, including the selection criteria and the importance assessment threshold (IRO-2). ESRS requires companies to disclose the importance assessment method used, the assumptions adopted, the focus and original information of the assessment process, as well as the judgment methods of quantitative/qualitative thresholds, reference standards, etc. ESRS 1 Appendix D provides the ESRS sustainable development reporting framework, while Appendix F provides specific cases for companies to understand how to disclose (see Figure 9).

Figure 9 ESRS 1 Appendix F

Other key points of the Implementation Guide

In addition to explaining how the EU ESRS defines importance, how the importance assessment process is carried out, and how to use other standards and frameworks, the "Guidelines for the Implementation of Importance Assessment" also answers common questions that companies may ask. In addition, the EFRAG website has set up a special ESRS Q&A platform to help collect and answer technical questions raised by stakeholders that have not yet been answered. On July 25, the EFRAG website published the latest version of the explanation of technical issues, and currently has a total of 93 explanations. Other key points raised in the frequently asked questions of the "Implementation Guidelines" are summarized as follows:

01Impact Importance Points

[Impacts caused by related activities and business relationships] The related activities of enterprises have an impact on stakeholders. "Related activities" include various forms. The impact caused by the operation and products/services of the enterprise should be the sole responsibility of the enterprise, such as employees working in a dangerous environment without safety measures; the impact caused by the participation of the enterprise, the enterprise's single action and no longer participating cannot reduce the impact, such as multiple factories polluting the local air environment, but the harmful gas emissions of a single factory are all below the harmful limit; the impact caused by the business relationship of the enterprise, the business relationship is not limited to contractual relationships and partners, but also includes the entire upstream and downstream value chain of first-tier suppliers and beyond, such as suppliers outsourcing the embroidery process of textiles to child labor. The negative impact caused by the business relationship of the enterprise is not necessarily "unimportant", but depends on the severity of the impact.

[Impacts cannot be offset by positive or negative impacts] ① Positive and negative impacts cannot be offset and need to be evaluated separately. They cannot be integrated due to the different nature and types of impacts; ② The time ranges corresponding to the impacts are different (for example, in the case of the same type of nature, the actual negative impacts of the current period cannot be offset by the positive impacts of the next few years), and the impacts of their own operations and the impacts of the upstream and downstream value chains cannot be offset; ③ Compensation/offsetting and netting are different concepts, but compensation/offsetting is not included in the impact significance assessment. There are some specific requirements for compensation/offsetting in the thematic ESRS. Please refer to the specific requirements of "ESRS E1 Climate Change" and "ESRS E4 Biodiversity and Ecosystems" for the disclosure of carbon credits and biodiversity credits for important topics.

02 Key points of financial importance

[Comparison of similarities and differences between financial materiality and financial reporting materiality] The materiality information in financial reports is different from the financial materiality information in sustainability reports, but the goal of information disclosure is the same. Decision makers who provide or may provide resources to the company in the future determine whether the information is financially material. The scope of financial materiality in sustainability reports is to further expand the scope of "material information" in corporate financial reports. The "European Union Sustainability Reporting Standards (ESRS)" and the "Financial Reporting Standards" have no difference in the concept of "materiality", but the definition of "materiality" information in the standards is different, and the threshold of financial materiality can refer to the recognition standards of accounting elements such as assets and income in financial reports.

Figure 10 Comparison of disclosures in financial reports and sustainable development reports

[Financial materiality is more proactive] Risks and opportunities that have not yet been identified as material in the financial report may be evaluated as material and displayed in the sustainable development report. This is because the recognition of resources/opportunities and risks is earlier than the recognition of assets and liabilities in the financial report.

[Risk Information] Potential future events may lead to the disclosure of expected risks and opportunities in the current sustainable development report, but financial reports generally only record risks that have occurred in the past period. Therefore, prospective information (such as expected financial impact) may be disclosed as important information in the sustainable development report.

[Relationship between financial materiality and financial impact in financial reports] The financial materiality (financial impact) of a sustainability report is not limited to the content disclosed in the financial report. According to the definition of financial impact in Annex 2 of the European Sustainability Reporting Standards (ESRS), it is divided into short-term financial impact (specified and confirmed in the financial report) and expected financial impact (not meeting the confirmation criteria and not included in the current financial report). The financial impact of certain ESG factors in the sustainability report has exceeded the information required to be confirmed and measured in the financial report and the notes to the financial statements.

03Other points

[Continuity of materiality assessment] The Corporate Sustainability Reporting Directive (CSRD) requires companies to publish sustainability reports every year. Companies can continue to use previous materiality assessment conclusions if they determine that there are no major organizational and operational changes and no changes in external factors (external factor changes refer to the generation of new or revised old IROs or the impact on certain disclosed information). Major changes include mergers and acquisitions, business/industry changes, major changes in the supply chain, the establishment of major new business relationships, the opening/closing of business lines or business areas, and changes in the definition of severity.

【Materiality Assessment and Information Integration of Group Companies】 ① If the group (parent company) is the disclosing party, it can adopt two methods or a combination of the two methods to conduct the materiality assessment process, from top to bottom ( assessment at the group level , communication with subsidiaries to obtain useful information) and from bottom to top (assessment at the subsidiary level, and aggregation of assessment results at the group level), and reasonably set the materiality threshold of IROs on a cross-industry/business basis to ensure the consistency of the methods used. ② If the group (parent company) is the disclosing party, it can appropriately integrate information based on relevant facts and circumstances on the premise that the content of important IROs is not confused. Enterprises should use separate integration standards for all IROs to reflect important information truthfully, fairly and accurately. For example, if the important IROs of different business regions/assets have a strong correlation with the business region/asset, enterprises should not integrate according to a higher-level integration dimension such as country to prevent enterprises from concealing important information or misleading report users in their judgment of materiality.

[Application order of important IROs] If an enterprise identifies a large number of IROs, it can prioritize them from the perspective of corporate management. From the perspective of report disclosure, the enterprise needs to disclose all important IROs, especially if the enterprise has not yet established a sound system, goals, and action plans to deal with these IROs.

[Data retention and subsequent application] The Corporate Sustainability Reporting Directive (CSRD) requires companies to conduct sustainability report attestation. Companies should retain information on the materiality assessment process of IROs to facilitate inquiries and use by attestation agencies and internal corporate management.

Comparison of relevant standards on ESG information disclosure

From the perspective of standards and criteria for ESG information disclosure, the dual materiality principle has been clearly adopted in the EU and my country (including Hong Kong). In contrast, the United States has not yet issued official sustainable development reporting standards. Its exchanges encourage flexibility in corporate assessments in terms of sustainable development reporting and allow companies to voluntarily disclose ESG information they deem important. The U.S. Securities and Exchange Commission (SEC) has always emphasized the disclosure of "important" information that investors are concerned about from a financial perspective in order to protect the rights and interests of investors. It only involves a small amount of ESG content. For example, the "Rules for Strengthening and Regulating Disclosure of Climate-Related Information to Investors" issued in March 2024 clearly stated the content that listed companies should disclose on climate change issues, which is a milestone.

Figure 11 Comparison of materiality principles adopted by multiple ESG information disclosure standards

summary

At present, although my country's three major exchanges and the Ministry of Finance have proposed the use of the "dual materiality" principle in the disclosure of sustainable development information, detailed operational rules have not yet been issued. The "Guidelines for the Implementation of Materiality Assessment" can provide valuable reference and guidance for Chinese companies in implementing this principle, helping them to better understand and apply it.

The "Corporate Sustainable Disclosure Standards - Basic Standards (Draft for Comments)" issued by my country's Ministry of Finance mentioned that the complete "Corporate Sustainable Disclosure Standards" will consist of basic standards, specific standards and application guidelines. Among them, the specific standards are similar to the "EU Sustainability Reporting Standards (ESRS)", which will include information disclosure requirements for sustainable topics in the environment, society and governance of enterprises; unlike the EU, industry information disclosure requirements will serve as the industry application guidelines of the Ministry of Finance, and the standard application guidelines are similar to the three "Implementation Guidelines" issued by EFRAG, which will explain, refine and provide examples for the basic standards and specific standards, and make operational provisions for key and difficult issues. In response to problems encountered by enterprises in the implementation of sustainable disclosure standards, the Ministry of Finance will provide Q&A on the implementation of the standards when necessary, and it is expected to jointly provide guidance for the release of sustainable development reports by listed companies on the three major exchanges.

The disclosure requirements of the EU ESRS standard and the first batch of EFRAG implementation guidelines are more detailed and practical than the Non-Financial Reporting Directive (NFRD), providing a normative reference for EU companies to use dual materiality as the ESG information disclosure principle, laying a solid foundation for the implementation of CSRD. At the same time, the implementation guidelines also provide ideas for ESG supervision and information disclosure in other countries and regions, and provide an effective reference for companies to optimize ESG management.